July 02, 2021

Form GSTR 6 is a monthly return statement for Input Service Distributor(ISD) to furnish the details of their distributed tax credit & inward supplies. GSTR6 format demands that the monthly return statement of the GSTR6 form has to be filed by organizations every month who are also input service distributors. It contains the details of Input Tax credit received and its distribution among the various organizations, along with the details of inward supplies received or purchased from registered taxpayers.

GSTR 6 form has to be filed by Input Service Distributor (ISD) after making an addition, correction, or deletion regarding the details of GSTR 6A. So most of the details in GSTR6 are auto-populated from the given details in GSTR6 form. Now let us proceed to know how to file GSTR06 in detail as per GSTR6 format.

We have several heads below under which information is required to be provided as per the GSTR6 return format.

Provide Goods and Service Taxpayer Identification Number (GSTIN) is a 15 digit number of the dealer for whom GSTR 6 monthly return is filed.

Name the taxpayer would be auto-populated.

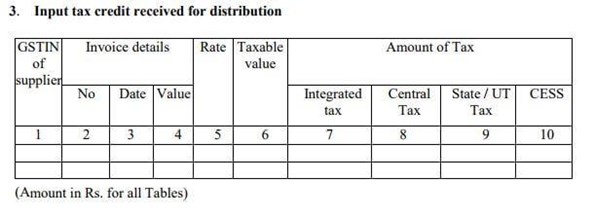

This section consists of invoice-wise details of the inputs received that are distributed as ITC.

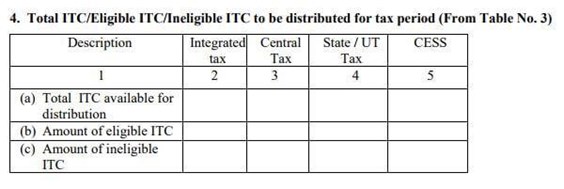

As per the GSTR6 format, this section consists of the total ITC of the ISD that is divided into eligible and ineligible ITC. Information here is auto-populated by table 3.

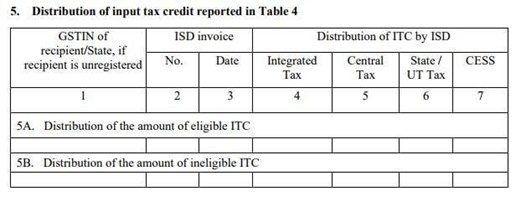

According to the GSTR6 format, the entire distribution of ITC is reported by the ISD in the return is mentioned under this head. The dealer who could claim the ITC would be able to do it based on this information with regards to the available credit under CGST, SGST and IGST comes under this head. It is needed to fill in the details of the invoice to complete the field.

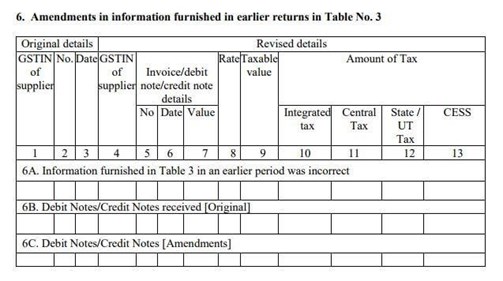

the invoice details of the inward supplies given in the previous returns and the information along with CGST/SGST and IGST charged could be corrected if there is any mistake in accordance with GSTR6 format.

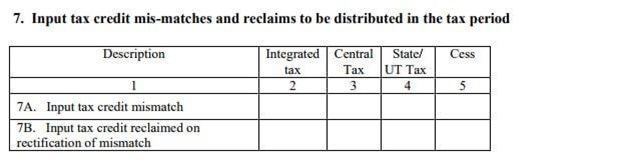

In the case of any modifications, mismatches or reclaims to be done in ITC under CGST, SGST, and IGST come under this head.

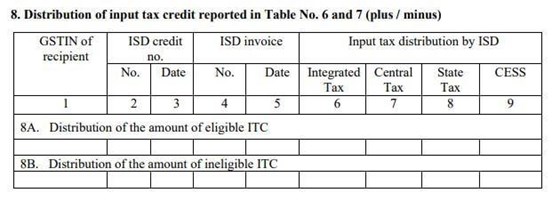

The modifications to be made to the amount of credit distributed to dealers for Table 6 or 7 under CGST, IGST and SGST could be entered here

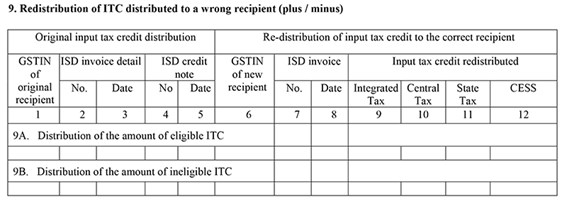

In case of any rectification regarding the distribution of ITC to the dealers in the previous returns, it could be entered under this head.

If there is any late fee payable or paid, details would be provided under this head.

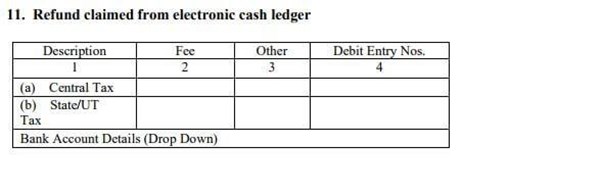

It covers the refund to be claimed from the electronic cash ledger.

At the end of the GSTR6 form after filing in the GSTR6 format, Input Service Distributor (ISD) is required to provide self-declaration by signing the form electronically to authenticate the information provided in the GSTR 6 form.

After filing GSTR6 return forms as per the GSTR6 return format successfully, an ARN would be generated. Then an SMS and an email id for acknowledgment would be sent to the applicant on his registered mobile number and email id. If there is any change or addition made in Form GSTR6, these details would be auto-populated in form GSTR-1 / 5 of the counterparty supplier.

As soon as the GSTR 1 Form / GSTR 5 Form gets successfully saved by the supplier, the auto-populated invoices would be reflecting in Form GSTR6A ( Table 3 and 4 ) and Form GSTR6 ( Tables 3, 6A, 6B, and 6C). An action could be considered on these invoices as soon as the GSTR 1 / 5 form has been submitted by the supplier.

Yes. An action on a compulsory basis is needed to be taken against all such invoices/CDN that have been auto-populated in Form GSTR6. Unless the taxpayer does so, that would make him unable to file GSTR6 Form.

Unless GSTR1 Form and GSTR5 Form got filled till the 10th of the following month of the tax period by the counterparties, no auto-population of the B2B details would be in Form GSTR6A and Form GSTR6 for the tax period. In such a scenario, it is the Input Service Distributor(ISD) who could modify the missing invoices /CDN by utilizing the function of ‘ADD MISSING INVOICE DETAILS /ADD CREDIT NOTE / DEBIT NOTE. These details would be at disposal under the table of ‘Uploaded by the supplier’. The uploaded B2B details could be flowing straight to the Form GSTR1/ Form GSTR5 of the suppliers.